Don’t sit on your Bankruptcy Eligiblity: It’s a moving target In January, Larry came to talk to me about Chapter 7 bankruptcy eligiblity. He had a car repossession and about $25,000 in charged off credit cards. He was planning to get married and hoped to...

Discharge in Chapter 13 is an Uphill Climb For most people, most of the time, getting a discharge is the goal of a bankruptcy case. The Supreme Court put it this way. “The principal purpose of the Bankruptcy Code is to grant a ‘fresh start’ to the ‘honest but...

What’s the Best Way to Try to Settle a Warrant in Debt? Do you want to avoid garnishment (and avoid bankruptcy) by negotiating your warrant in debt? I get asked about that a lot. So here’s my best advice. Go to court and Ask for a Trial It doesn’t...

It’s Already Three Months Since Your Bankruptcy Discharge How are you doing? Did bankruptcy work out the way you expected? Are you in control of your life, now? I claim that after bankruptcy you will sleep better, you’ll be happier, your credit score will...

How Quickly Does the Postal Service Deliver Your Chapter 13 payment? When you are in Chapter 13, you need to make your monthly trustee payments on time–especially in the first four months of the case. So it doesn’t help that our Chapter 13 Trustee in...

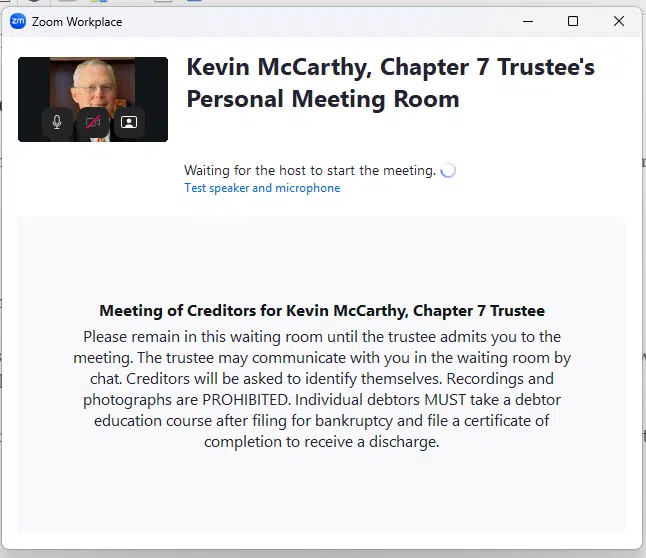

Chapter 7 Trustee Kevin McCarthy Kevin McCarthy is one of the four Chapter 7 trustees in the Alexandria, Virginia, Bankruptcy court. When you file a bankruptcy case in Alexandria, the computer assigns you to one of the four trustees. Lawyers work as Chapter 7 trustees...